InsurAce.io are delighted to confirm that we have implemented the first phase of V2 with some initial product launches.

We are delighted to publish the long-awaited InsurAce.io V2 litepaper and to confirm the launch of new product features for the first phase of V2.

InsurAce.io has today officially published the V2 litepaper, laying out the core designs and future roadmap of InsurAce.io to the next level. Meanwhile, the first batch of V2 product features has been deployed. It is important to note that future phases will be launched over the coming months.

How did we get here?

InsurAce.io V1 has been live for 10 months and has experienced notable growth in such a short space of time. The growth has continued while InsurAce.io has been at the forefront of innovation.

The journey started during the DeFi summer of 2020. The team noticed a need for better and more insurance products as crypto continued to boom. InsurAce.io was founded as the first multi-chain protocol providing insurance products to crypto users regardless of economic status and chain of choice.

Launching to the Ethereum mainnet in April 2021, InsurAce.io subsequently expanded onto BNB Chain, Polygon and Avalanche, offering the easiest and broadest access for users in this multi-chain space. In 2022, InsurAce.io has already received development grants to expand onto Harmony, NEAR and Aurora, as well as being incubated into BNB Chain’s Most Valuable Builder (MVB) program.

InsurAce.io v1 offered 4 types of insurance cover including smart contract vulnerability, stablecoin de-peg, IDO risk and custodian risk, with its unique portfolio-based coverage and customized bundled covers.

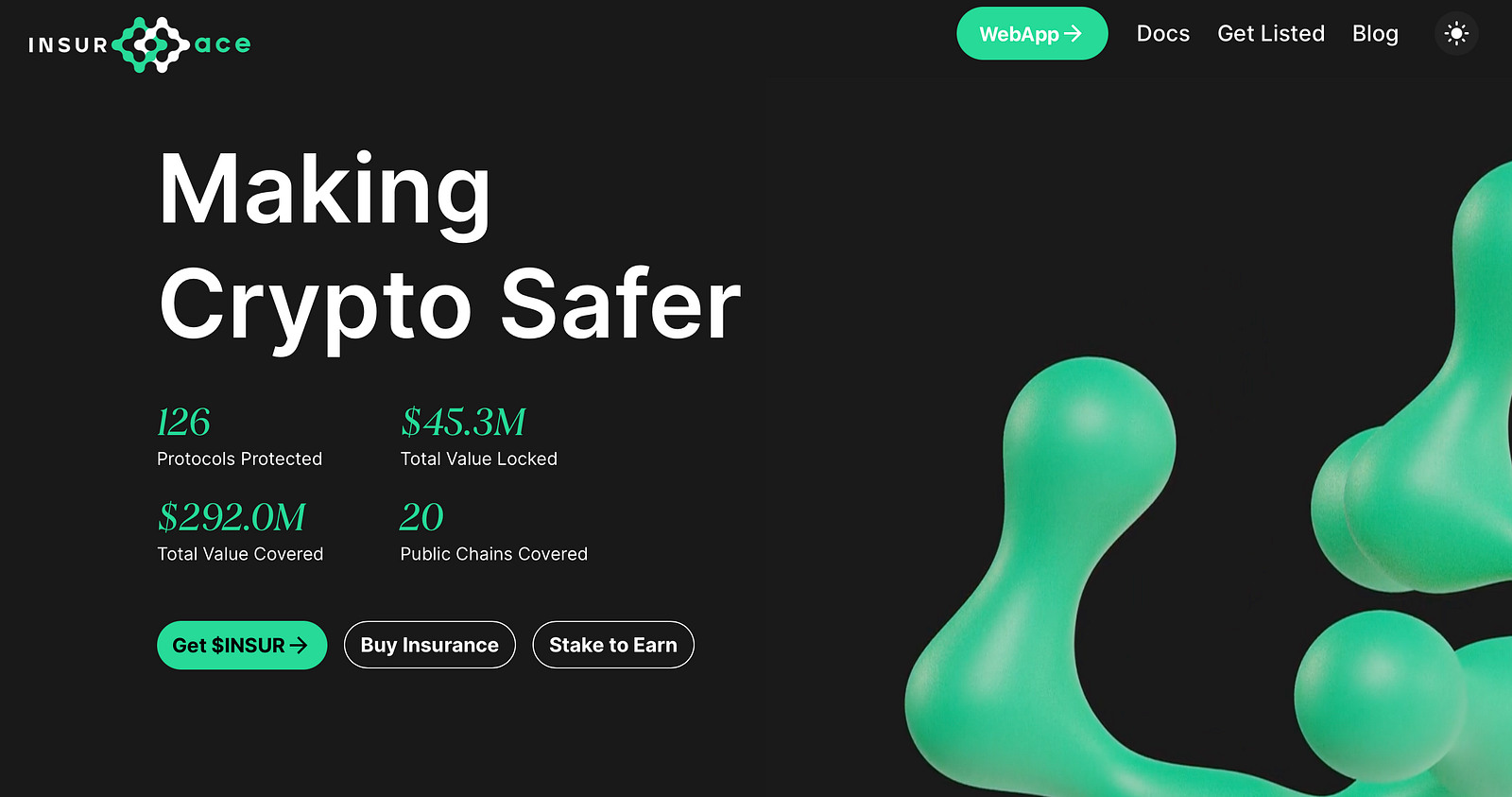

InsurAce.io has experienced extraordinary growth, as of the time of writing, InsurAce.io currently protects 130+ protocols, across 19+ public chains with a total of 280m+ in TVC (Total Value Covered), 3200 covers sold, with monthly premium earnings of around 200K.

InsurAce.io v1 offered 4 types of insurance cover including smart contract vulnerability, stablecoin de-peg, IDO risk and custodian risk, with its unique portfolio-based coverage and customized bundled covers.

InsurAce.io has also accumulated 40k+ total users and 11k+ token holders. On top of this, InsurAce.io has secured 60+ partnerships with a global community of over 100k+. Undoubtedly, InsurAce.io has now grown to be the leading multi-chain DeFi insurance protocol.

So why do we need InsurAce.io V2?

During the process of building and operating V1, InsurAce.io has seen a strong and rapidly growing demand for insurance products. This has been emphasised with $2.6bn (according to Immunefi annual summary) being recorded as lost due to smart contract vulnerabilities in 2021 alone. Of that, less than 5% was covered by insurance.

It has also been noticed that alternative risks are on the rise, such as exploits of the front-end, NFT and centralized exchanges. The industry is still growing at an extremely fast pace which will lead to more risks being exposed.

Insurance can play a key role in managing these risks and the learnings on development from InsurAce.io V1 that not all existing challenges have been properly addressed.

InsurAce.io V1 still has challenges such as:

- Misaligned token incentives

- Insufficient cover capacity

- Demand for broader offerings

- Wider and seamless access for more users

These challenges are not separate but interconnected. V2 is a systematic approach to address these issues through an improved protocol, including:

- Revised tokenomics

- Increased capital efficiency and insurance capacity

- Releasing innovative new insurance products

- Continue to expand in multi-chains.

InsurAce V2 aims to bring insurance to the forefront of Web3. It is an ambitious endeavor to rapidly innovate to protect investors and to allow them to be well on their way to securing Web3 prior to onboarding the next billion users.

InsurAce V2 plans to achieve this mission through an improved protocol, revised tokenomics, increased capital efficiency and releasing innovative new insurance products, all in a multi-chain setting.

Further information can be found via our litepaper: https://files.insurace.io/public/InsurAceV2Litepaper.pdf

So, what is coming?

As previously mentioned, V2 is going to be a phased launch given its broad scope and high complexity. The plan will be:

- 1st Batch (Q1): multi-chain insurance aggregator, cover cancellation, dynamic pricing, public API access, new data reporting system, and new landing page.

- 2nd Batch (Q2): revised tokenomics to a veINSUR model with governance portal, underwriting capacity expansion measures, and treasury module.

- 3rd Batch (Q3): Investment arm, new insurance product offerings, and insurance marketplace.

The first set of implementations was deployed on March 29th, 2022.

Multi-chain Insurance Aggregators

The first release will involve the aggregator. With the prosperity of new public chains beginning in Q2 2021, DeFi quickly evolved and took shape on alternate chains, pulling in more capital, users, and builders into these new ecosystems. This is why V1 was launched quickly onto 4 chains.

Due to this, it helped insurAce.io acquire more TVL, cover sales and new users. InsurAce.io will continue to build more chains in 2 and quickly bring these services to incumbent users. The following is how it would work:

Capital aggregation

Before aggregation: the capital pools are segregated among different chains. For example, the capital staked on Ethereum network will only be used to underwrite risks for covers purchased on Ethereum.

After aggregation: The capital from all chains is aggregated to be used for risk underwriting. Increased underwriting ability thus help to provide more capacity.

Capacity aggregation

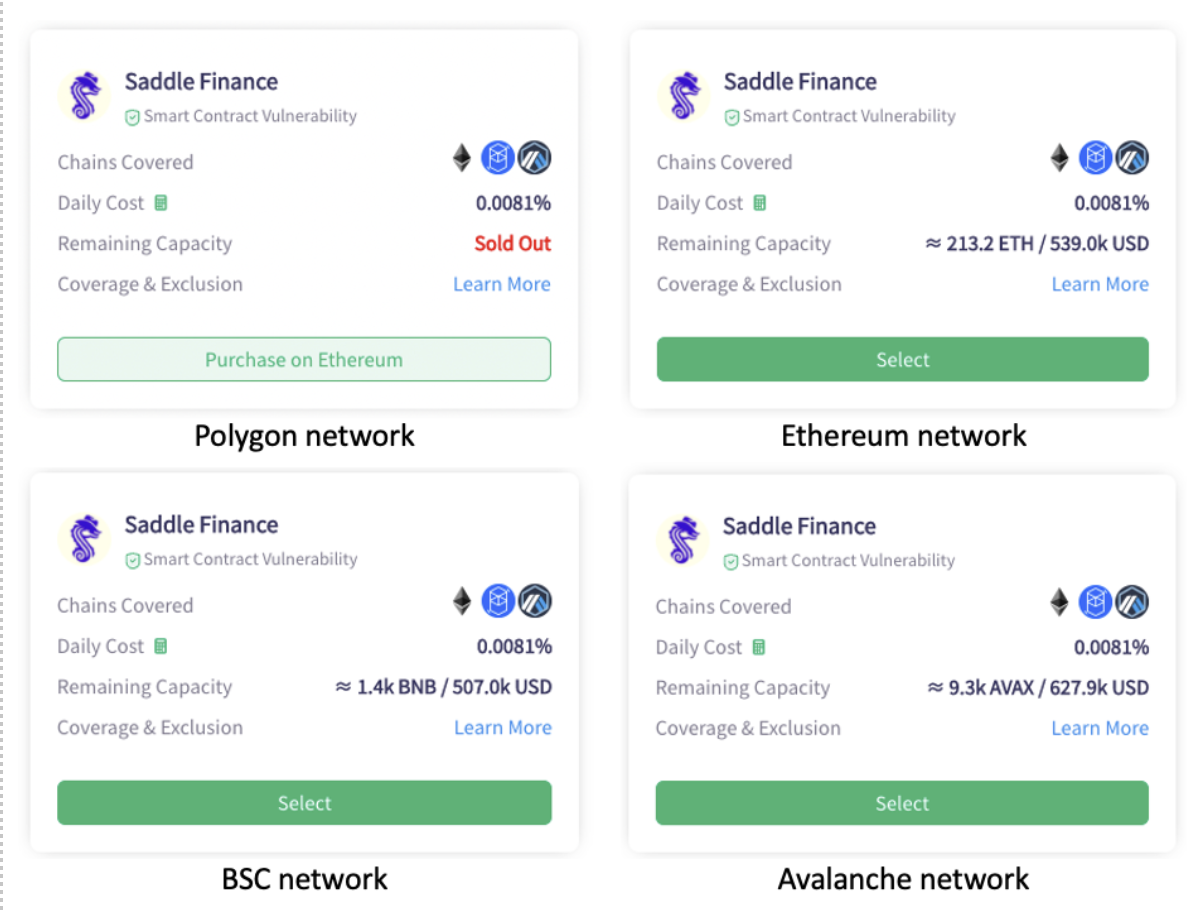

Before aggregation: The capacity is segregated among different chains and be constrained by the TVL on each chain. Users need to toggle between chains to view the capacity on different chains. Moreover, if the product is sold out on chain A, users have no choice but to bridge their assets to purchase through other chains.

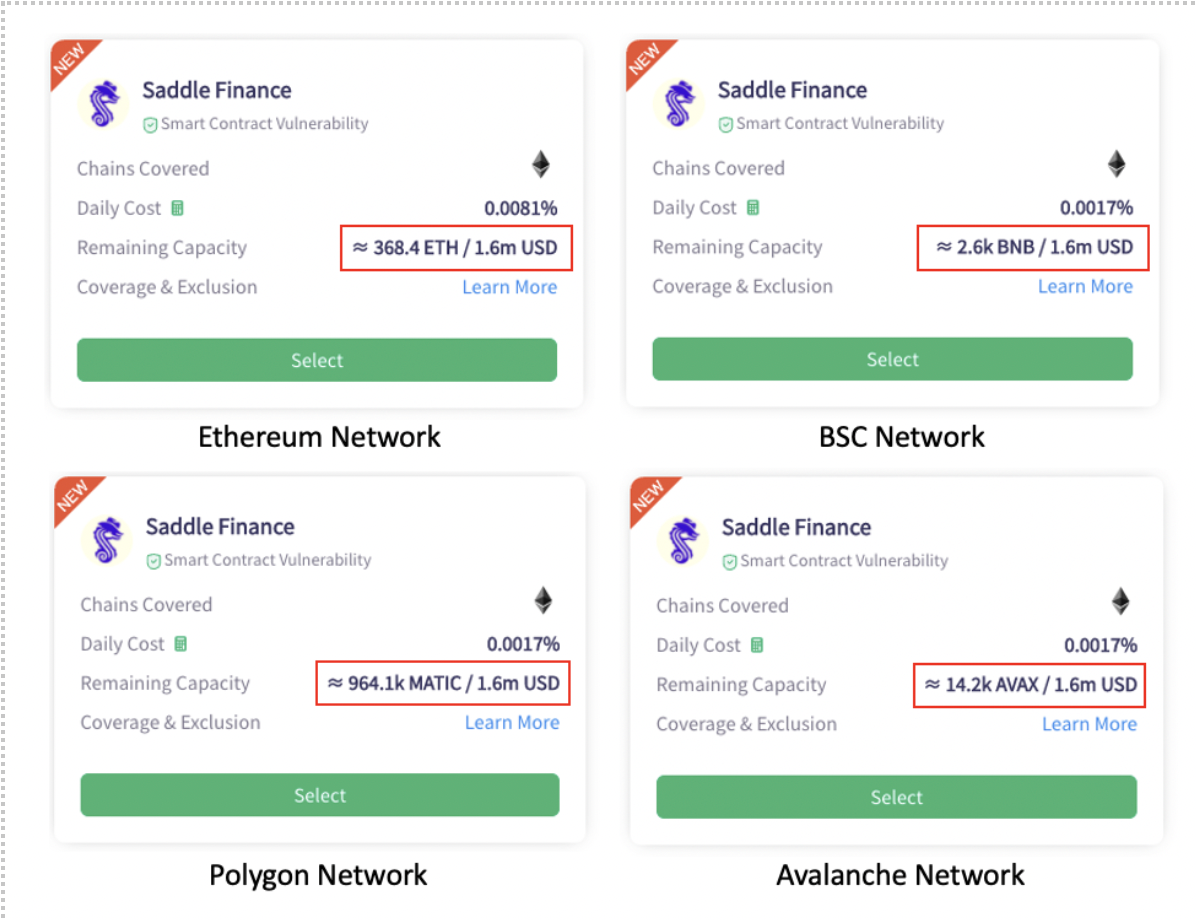

After aggregation: Users can view and get access to the full capacity through any chains. If previously they can only purchase $1M cover through Ethereum network, now they might be able to purchase $4M cover through Ethereum network. This helps to enhance the user experience and attract more whale users.

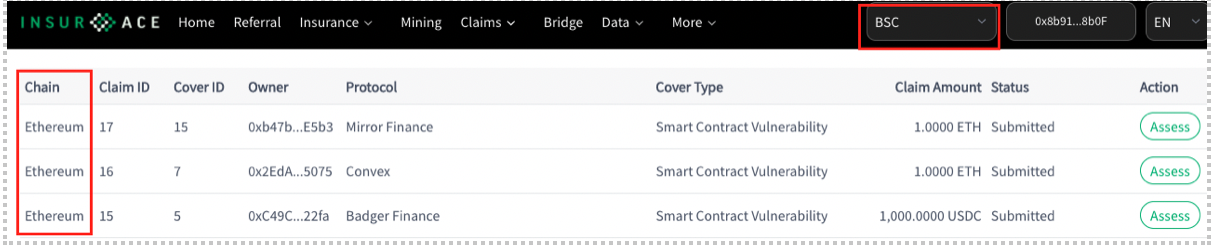

Claim voting across multiple chains

Before aggregation: A claim filed on chain A can only be assessed by claim assessors staking INSUR on chain A. Users need to toggle between chains to view the claim on different chains.

After aggregation: The claim can be viewed and assessed by users across chains. No need for claim assessors to bridge INSUR for voting on different chains.

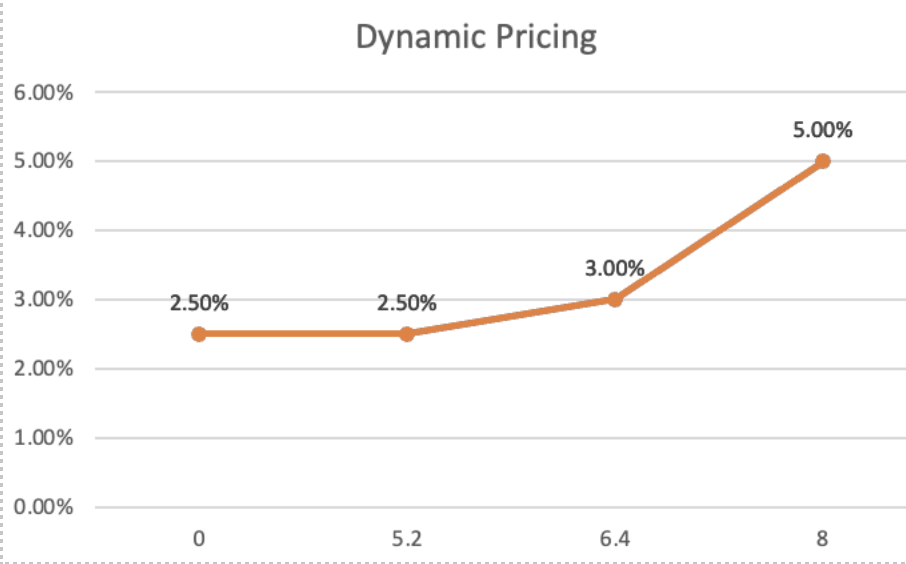

Dynamic Pricing

Dynamic pricing has been set up in V2 to price risk in a fairer manner based on the supply-demand curve, and further boost the cover sales. With more revenue, we will be able to support more capacity for the cover offerings, and eventually, capture more value for the tokens.

Implementation: The premium will be determined by the supply and demand for that cover product, changing between a minimum price and a maximum price. The more the product is sold, the higher the premium and vice-versa.

For each product, we will increase its total capacity by around 50%. The premium for the original capacity which is around 65% of the current total capacity will remain unchanged. The premium for the added capacity will increase following our dynamic pricing model.

Below is an example. The number used there is just for illustration purposes. Actual settings for each cover product are subject to change.

Example: Original capacity 5M with an annual premium of 2.5%. Now total capacity increased to 8M.

– Premium for the first 65% sold (5.2M) will be 2.5% unchanged.

– Premium for the remaining will gradually increase to a max of 2x base premium (5%+) when 100% is sold.

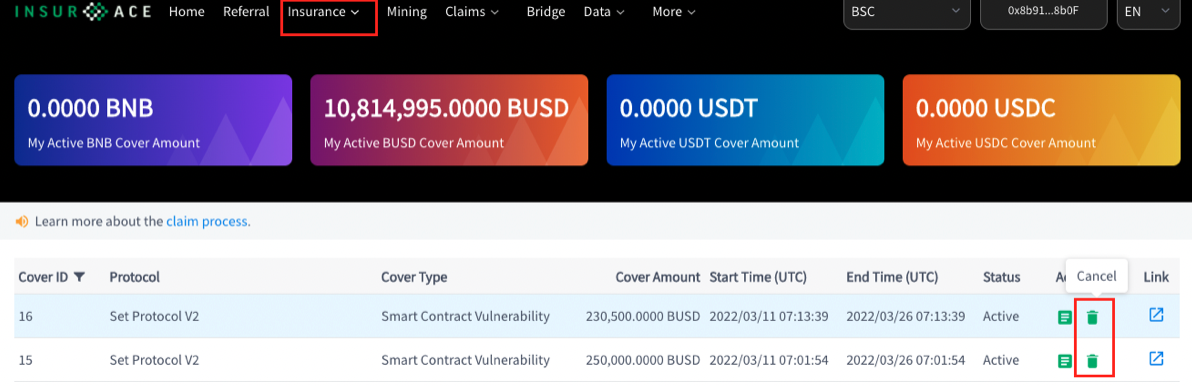

Cover Cancellation

We now support on-chain cover cancellation function, a long-awaited feature for our users. Navigate from the top menu “insurance” to sub-menu “active covers” and now you will see the option to cancel.

A cancellation fee of 5% of the premium paid will be charged forcover cancellation. We will then refund the remaining unused premium in INSUR token with deduction of any cover rewards given to the user and the referrer if a referral code was used at the time of purchasing the cover. This cancellation fee is an initial setting and will be subject to governance once the portal is live.

Public API Access

InsurAce.io officially launched the API in November 2021, aiming to bring insurance services to the forefront of DeFi services. This feature was only for whitelisted projects and service partners to integrate with our dApp.

We have now opened our API to the public, allowing all users to access our services through API easily. The list of services supported by our API can be found here: https://docs.insurace.io/landing-page/developer-reference/service-integration

There is a public shared API key provided in the documents from the link above. For project teams, institutional users or others who need larger traffic, please request via this form: API Key Request Form

If you have any questions or need any technical help, our team will continue to be available via our social channels below.

Join InsurAce.io community:

Website | Twitter | Telegram | LinkedIn | Announcements | Medium

The status quo of DeFi insurance is quite different from the extensive nature of insurance in traditional finance and has yet to improve relative to other DeFi verticals. Web3 and DeFi’s expansion will continue and thus our services and infrastructure must adapt. We hope with the fully launch of v2, InsurAce.io will advance further to be the leading insurance protocol, securing the whole Web3 space and creating substantial values for our users, token holders and community